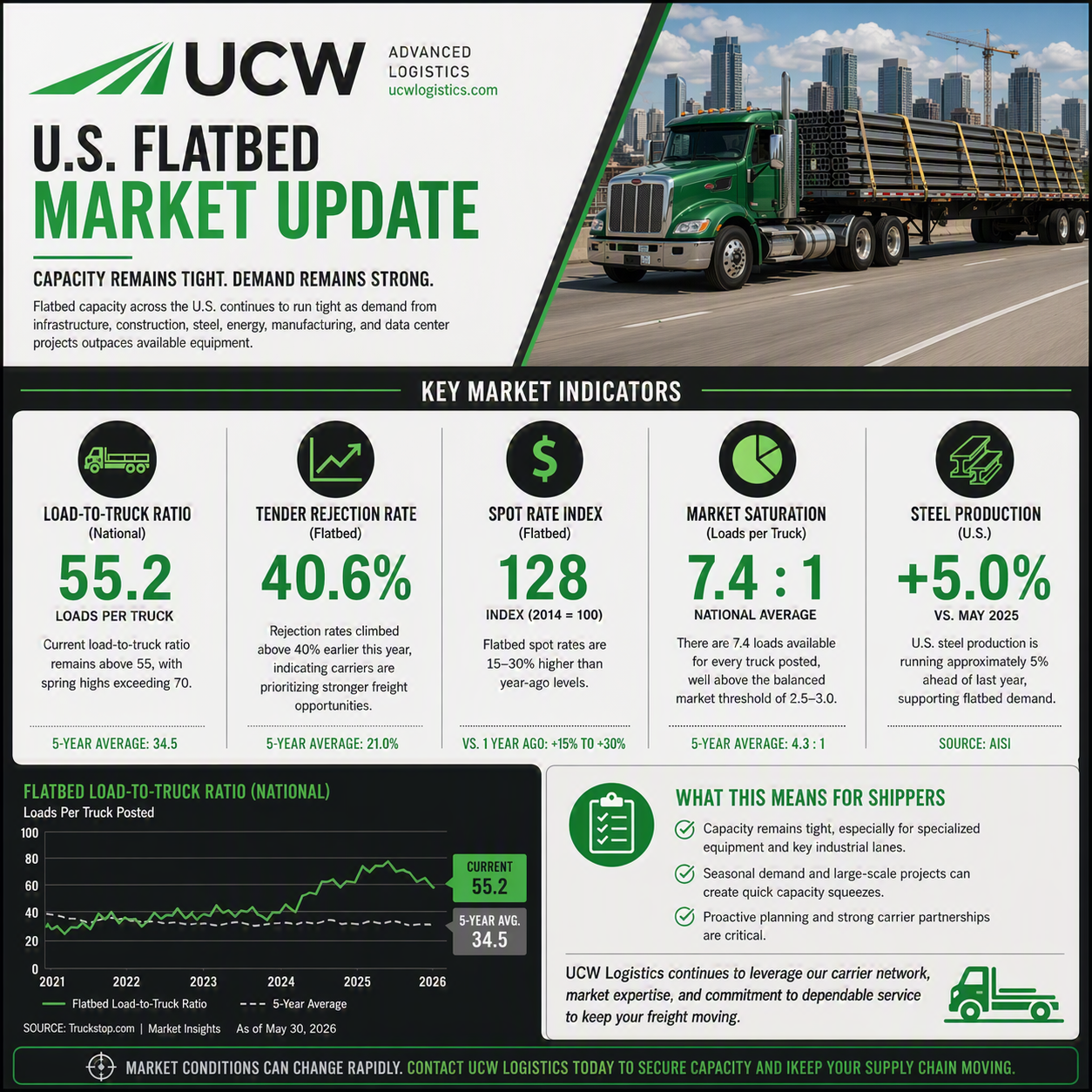

State of U.S. Flatbed Capacity: Summer 2026

Flatbed trucking capacity remains relatively tight across the U.S., supported by ongoing demand from infrastructure projects, steel production, energy, manufacturing, and data center construction. Industry data shows the national flatbed load-to-truck ratio recently remained above 55 loads for every truck posted, with spring highs exceeding 70 loads per truck—nearly 60% above the five-year average. At the same time, flatbed spot rates are running approximately 15-30% higher than year-ago levels, signaling a market where demand continues to outpace available capacity in many regions.

While some construction segments have begun to soften, capacity remains susceptible to seasonal tightening. Earlier this year, flatbed tender rejection rates climbed above 40%, indicating carriers were turning down contracted freight in favor of stronger opportunities in the spot market. Steel output is also running roughly 5% ahead of last year, helping sustain freight demand across key industrial corridors. For shippers, these trends reinforce the importance of securing capacity early and partnering with providers that have access to a resilient carrier network. At UCW Logistics, we continue to monitor market conditions closely to help customers stay ahead of capacity constraints and keep freight moving efficiently.